From a young age, we are taught that keeping money in the bank is safer than hiding it under a mattress. But for cash to retain its value, it must earn more in interest than the rate of inflation. When it fails to do so, its purchasing power is steadily eroded.

The period between 2021 and 2023 provided a stark reminder of this reality. As UK inflation surged to a 41-year high of 11.1% in October 2022, interest rates struggled to keep pace, leaving savers’ cash exposed. In response, the Bank of England raised its base rate repeatedly, reaching a peak of 5.00% in October 2024.

However, the economic landscape has shifted again. With inflation falling, the Bank has reversed course, cutting the base rate four times to its current level of 4.00% as of August 2025. Forecasts suggest this downward trend will continue, with economists predicting the base rate could fall to between 3.5% and 3.75% by the end of 2025. In this environment, savers must once again be vigilant in protecting their cash from eroding in value.

Gold vs other assets

During the recent period of economic uncertainty and high inflation, gold has demonstrated its historic role as a store of value. Driven by a flight to safety amid global economic and geopolitical tensions, the precious metal has reached new heights.

On April 22, 2025, gold achieved a new nominal all-time high in British Pounds, reaching £2,610.22 per troy ounce. Globally, the price surged past $4,000 per ounce for the first time in October 2025.

In contrast, cash held in savings accounts has struggled. As of October 2025, the average interest rate for an easy-access savings account had fallen to approximately 2.68% AER. With the inflation rate at 3.8% in September 2025, the real value of money in these accounts is actively decreasing.

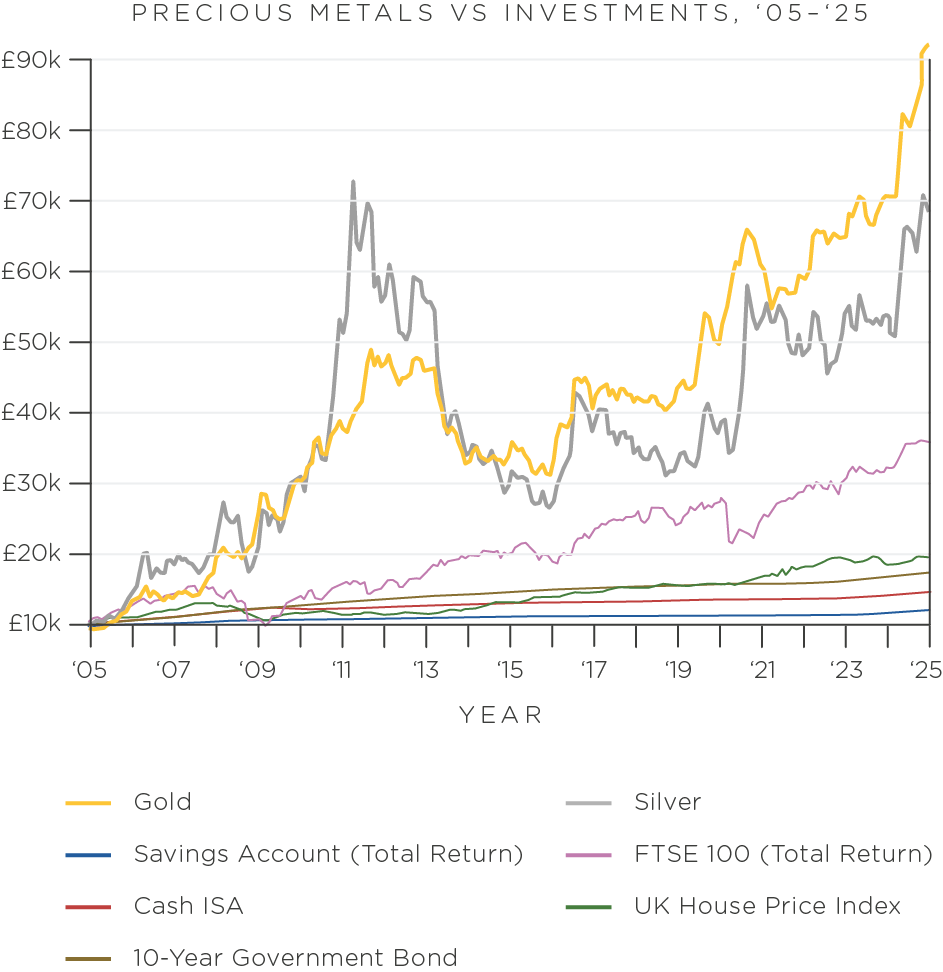

Gold vs other assets

This graph tracks how much an investment made in January 2005 of £10,000 in gold or a bank savings account would be worth.

Cash left in a savings account for the same period:

- would be worth £12,114, the worst-performing investment choice.

As you can see, £10k invested in gold:

- would have been worth £92,468k in January 2025, significantly more than the rise in inflation.

Why Banks?

Banks began as institutions that existed to store money. They are one of the linchpins of the global economy, with the interest rates they offer being a matter of concern for national governments and financial institutions. In conventional wisdom, banks are the place to store cash, as well as other financial instruments and asset classes.

Banks want more capital to invest for profit, and they provide a useful service to customers. Storing wealth in the bank is convenient in the short term and reasonably secure from external theft, as advanced encryption protects a customer’s money. However, the very nature of banking and currency is evolving, with projects like the Bank of England’s “Digital Pound” signalling potential future shifts in the financial system, with a decision on its implementation expected around 2027.

Comparing Banks & Gold

RISK

Gold

Owning physical gold comes as close to eliminating counterparty risk as possible. It is a tangible asset that you hold directly. If it is to be stored, it can be held in an allocated, segregated vault under your ownership, and if it is stored securely at home then the only risk is theft.

Banks

The 2008 Global Financial Crisis showed that even large financial institutions can fail in times of extreme economic stress. It is clear now that even major banks come with an element of counterparty risk. While the aftermath of the crisis has brought greater checks on the solvency of banks, some risk remains in every contractual agreement, including holding cash in the bank.

INFLATION

Gold

There is a finite supply of gold, it has been a safe-haven asset for centuries, and the metal is in high demand during times of political and economic uncertainty. This means that gold’s value is likely to increase over the long term. General fluctuations in price are expected, but as a tangible commodity, it tends to rise alongside other goods, making it a powerful hedge against inflation.

Banks

The rising price of goods erodes the value of any cash you hold. Unless the interest you receive on bank deposits is greater than inflation, your money will be worth less when you come to spend it.

While inflation has fallen from its 40-year peak, it remains a persistent threat to savers. Average easy-access savings rates have fallen to just 2.68% AER, while inflation stood at 3.8% in September 2025. This negative real return means the purchasing power of cash in the bank is being eroded quickly. Even the top 1-year fixed-rate bonds offer rates that may struggle to deliver significant real returns in the current climate.

LIQUIDITY

Gold

Gold holds very similar liquidity benefits to cash. It is easily liquidated (with a buy-back guarantee, some gold can be liquidated within 24 hours), and it can be sold anywhere around the world. It is not as immediate as withdrawing cash from an ATM, but it is almost as quick to turn physical gold back into cash.

Banks

Often the main reason for keeping cash in the bank is for easy access when opportunities for investment arise. Investors can withdraw cash immediately, and this allows them flexibility to respond to changes in the market.

Looking Into Gold Investment?

Book a FREE consultation with our expert brokers at The Pure Gold Company.

Explore more gold comparisons

You might also like to read:

Learn more about getting into gold investment with our detailed guide on How to invest in Gold